Do you know how to quickly confirm whether your indirect rates are complete? Did you know that your indirect rate report may not be accurate? That’s right, even if your accounting system helps with this, it could be missing something in the setup. One of the most important calculations a GovCon makes is setting and monitoring indirect rates. The result may be that you rely on an indirect rate report to support pricing that is not correct. Make it a regular step in your closing process to check whether your indirect expense report includes all of the costs that it should in the calculation.

Indirect costs encompass what is also referred to as overhead expenses, such as rent and utilities, or general and administrative expenses, such as HR, accounting costs and executive salaries. The purpose of indirect rates is to allow your company to recover the proportion of these costs attributable to each project. If your report is off, you may be relying on incorrect indirect rates when you set your strategies for bidding on contracts as well as spending on your business.

Two Formulas Help Cull the Culprits

When CAVU evaluates a client’s data, we run the following quick check that includes indirect rate input (stay tuned for another important data check in our next blog).

It is surprising how many times the indirect rate report does not reconcile to the income statement. Why would this happen? The biggest culprits are:

- Indirect rate formulas do not include newly-added accounts.

- The formulas themselves are just wrong.

Even if you have an accounting system that supports indirect rate calculations, do not automatically assume that the rates are correct. Check that they are at least complete by using the formulas below for a standard total cost input base and a value-added base.

Total Cost Input Base

This is your typical three-tiered rate structure with fringe, overhead(s), and general and administrative (G&A) rates.

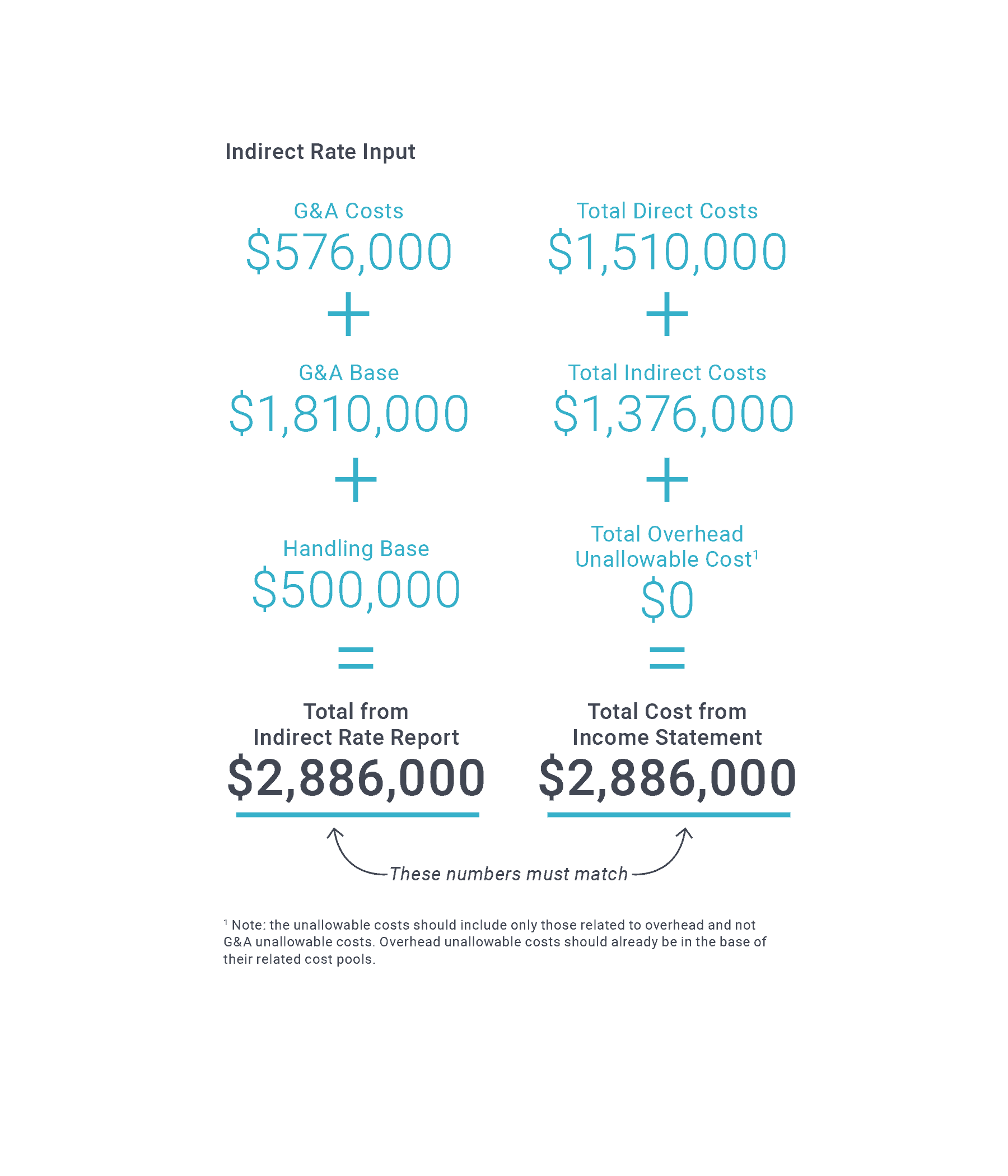

Value Added Base

This is a cost pool with a separate handling pool such as a Material and Subcontract Handling pool (M&S Handling). This cost pool can be set up for only one category, such as Material Handling or Subcontract Handling. In the formula below, the base of the handling pool must be added to the indirect rate input. Note that you do not add the handling pool cost. The handling pool cost should already be in the G&A pool base.

If you are still unsure that your indirect expense report includes all of the costs, you should call for backup from CAVU’s experienced GovCon accountants. We can help you confidently navigate rate-setting complexities for solid bids and financial planning that meet your federal agency clients’ requirements and earn you a profit to boot.

If you are still unsure that your indirect expense report includes all of the costs, you should call for backup from CAVU’s experienced GovCon accountants. We can help you confidently navigate rate-setting complexities for solid bids and financial planning that meet your federal agency clients’ requirements and earn you a profit to boot.